The Next Evolution: What Remote Closing 2.0 Means for Lenders and Borrowers

A futuristic remote mortgage closing scene showing a borrower and lender interacting digitally, with AI, biometric verification, eVaults, and holographic home elements highlighting the secure, seamless Remote Closing 2.0 experience.

How AI Digital Twins of Borrowers Will Transform Risk Modeling

AI-driven digital twins give lenders real-time insight into borrower behavior, improving risk modeling, predicting defaults earlier, and enabling smarter, more personalized underwriting and servicing decisions.

Smart Compliance: How AI Monitors Every Loan in Real Time

Smart compliance powered by AI helps lenders monitor every loan in real time, catch issues early, and close faster with lower compliance risk.

Machine-Generated Pooling Reports: The End of Manual Aggregation

Machine-generated pooling reports eliminate manual data aggregation, delivering faster, more accurate, and investor-ready loan pool summaries through automation, real-time validation, and seamless secondary-market integration.

AI-Powered Personalized Mortgage Offers: A Smarter Way to Borrow

Discover how AI-powered personalized mortgage offers match borrowers with smarter rates, flexible terms, and faster approvals.

Smart Contracts for Mortgage Closings: Are We Ready for Self-Executing Loans?

Smart contracts are transforming mortgage closings with automation, transparency, and faster workflows. Learn how blockchain-enabled self-executing loans could reshape the future of digital lending.

Subscription-Based Mortgage Services: The Next Business Model Shift

A futuristic illustration showing a home centered within a digital subscription platform, highlighting tiered mortgage plans, recurring payments, and technology-driven services shaping the future of mortgage lending.

Zero-Trust Architecture as a Federal Requirement: What Lenders Should Expect

A futuristic visual showcasing Zero-Trust Architecture as a federal mandate, highlighting identity verification, data security, compliance controls, and vendor security—illustrated through glowing digital interfaces and a lender reviewing cybersecurity frameworks.

The Role of Smart eNotes in Accelerating Secondary Market Trades

The secondary mortgage market depends on speed, accuracy, and trust. Traditionally, transferring mortgage loans between lenders and investors involved paper notes, manual reviews, and long settlement times. Today, smart eNotes are transforming this process by making secondary market trades faster and more secure.

Tokenized Mortgages: How Blockchain Will Open New Investment Channels

The mortgage industry is going through a quiet but powerful transformation. One of the most exciting changes on the horizon is tokenized mortgages—a concept that combines real estate, mortgages, and blockchain technology.

The Future of Data Syndication for Investors and Regulators

In today’s digital financial ecosystem, data is no longer just information—it is an asset. Investors depend on reliable data to make confident decisions, while regulators require accurate reporting to maintain market stability.

How AI Advisors Will Reduce Dependence on Loan Officers

For decades, loan officers have been the main guides for borrowers navigating the mortgage process. From explaining loan options to collecting documents and answering questions, almost every step relied on human support. But today, AI advisors are changing that model.

Continuous KYC: Ongoing Borrower Verification for Risk Reduction

In today’s fast-changing financial world, lenders can’t rely on a one-time identity check anymore. Borrowers’ financial situations shift, risks evolve, and fraud methods become more sophisticated. This is why Continuous KYC (Know Your Customer) is becoming essential in modern mortgage and lending systems.

The Rise of Predictive Servicing: Stopping Defaults Before They Happen

In the mortgage industry, servicing has traditionally been reactive. Lenders and servicers often step in after a borrower misses payments or shows clear signs of distress. But today, that approach is changing. Thanks to data, analytics, and AI, a new model is emerging—predictive servicing.

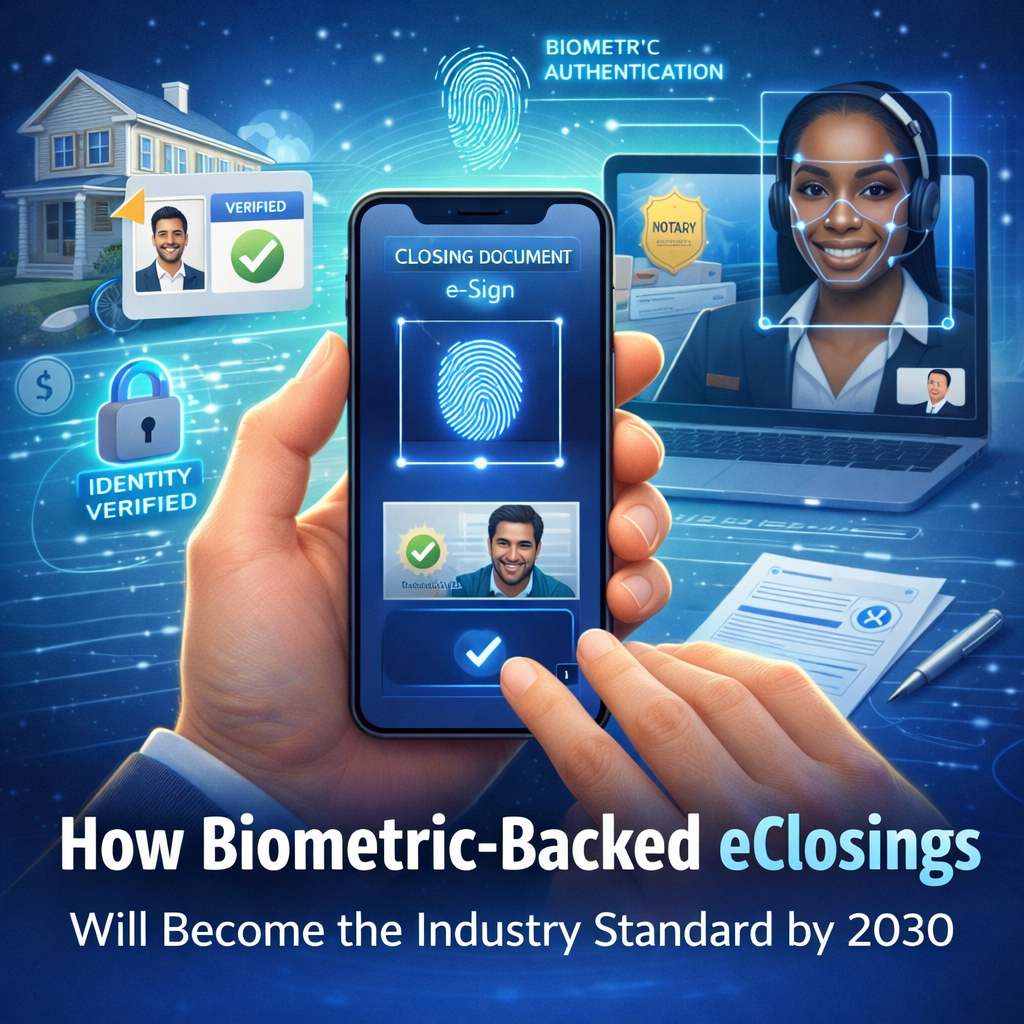

How Biometric-Backed eClosings Will Become the Industry Standard by 2030

The mortgage closing process has always been known for paperwork, in-person meetings, and long wait times. But by 2030, that experience will look completely different. Biometric-backed eClosings—closings supported by digital identity checks like facial recognition, fingerprint scanning, and voice verification—are set to become the industry standard across the U.S.

Predictive Loan Trading: How AI Will Optimize Secondary Market Decisions

The secondary mortgage market plays a crucial role in keeping lending liquid. Lenders sell loans, investors buy them, and capital flows back into new lending. But deciding when to sell, what to sell, and at what price has always been complex and data-heavy.

The Next Generation of MISMO Standards: What Lenders Must Prepare For

The mortgage industry runs on data—and MISMO standards are what keep that data consistent, reliable, and usable across systems. As digital mortgages, automation, and AI adoption accelerate, MISMO is evolving to support the next generation of lending.

Self-Service Mortgage Portals: The Future of Borrower Empowerment

The mortgage world is changing fast. Borrowers today expect the same convenience they get from online shopping, food delivery apps, or digital banking. That’s why self-service mortgage portals are becoming a core part of the lending experience.

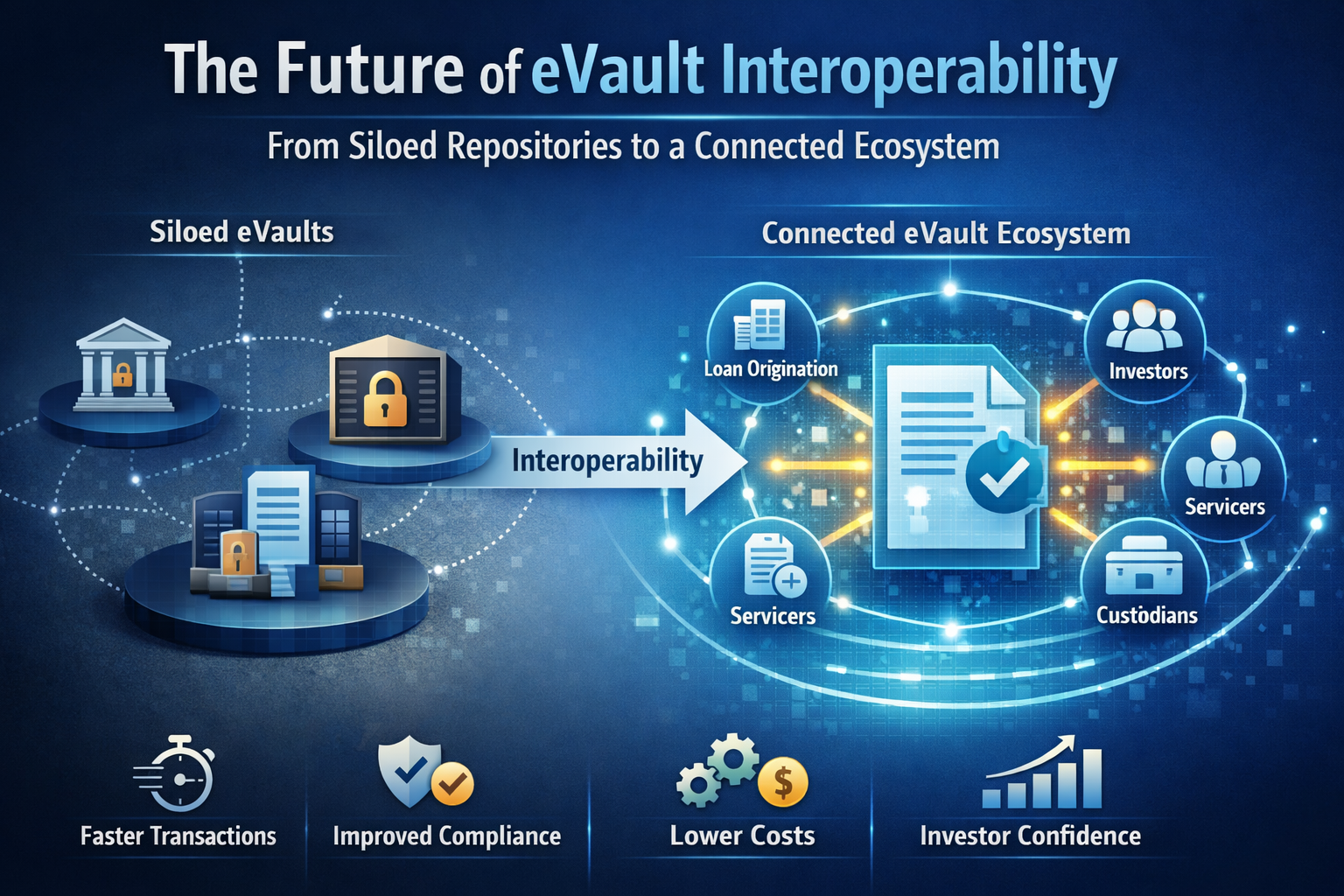

The Future of eVault Interoperability: From Siloed Repositories to a Connected Ecosystem

As the mortgage industry continues to go digital, eVaults have become a critical part of how lenders store, manage, and transfer electronic loan documents—especially eNotes. However, while eVault adoption has grown, many systems still operate in isolation. This lack of connectivity creates delays, risks, and inefficiencies.

The Rise of AI Underwriters: What U.S. Borrowers Should Expect by 2030

The underwriting process has always been one of the most time-consuming and stressful parts of getting a mortgage. Borrowers wait days—or even weeks—for someone to verify documents, calculate risk, and make a decision.