Blockchain in Mortgage Lending: From Security to Speed

Blockchain has moved far beyond the world of cryptocurrency—today, it’s transforming industries that rely on secure, high-value transactions. Mortgage lending is one of them. As lenders, investors, and regulators push for faster processing, stronger data security, and end-to-end transparency, blockchain technology is emerging as a powerful tool to modernize the mortgage ecosystem.

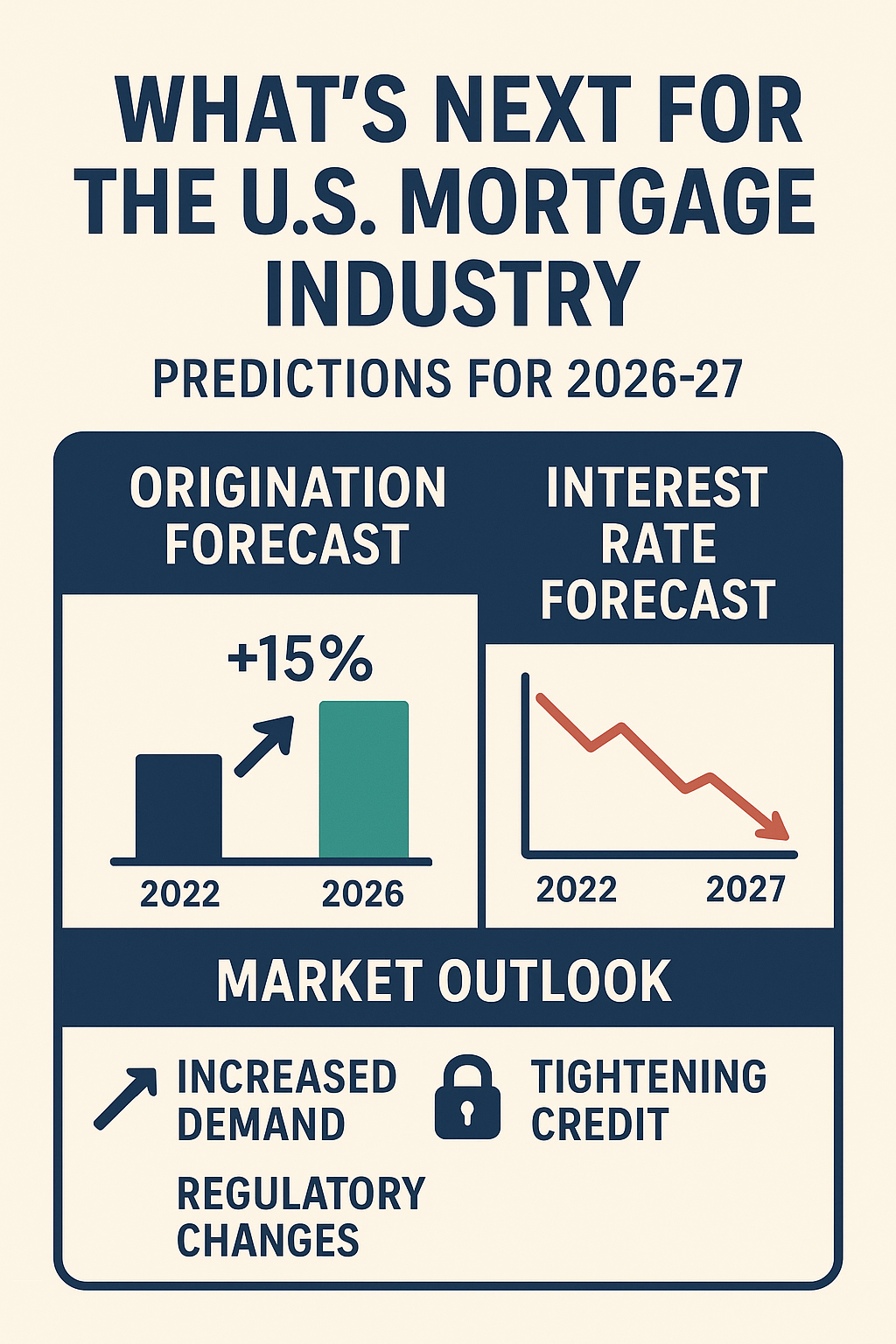

What’s Next for the U.S. Mortgage Industry: Predictions for 2026–27

The U.S. mortgage industry is heading into a period of major transformation. After several years of volatility—historic rate hikes, affordability challenges, low housing supply, and shifting borrower expectations—lenders are now preparing for what 2026–27 may bring.

Meeting ESG Standards in Mortgage Lending: Why It Matters in 2025 and Beyond

The mortgage industry is undergoing a major transformation — not just digitally, but ethically. As investors, regulators, and borrowers become more focused on sustainability and responsible business practices, ESG (Environmental, Social, and Governance) standards have become a central part of how lenders operate.

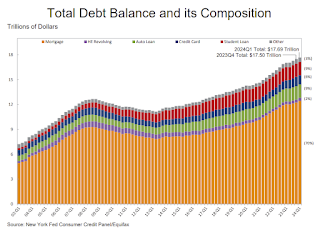

Delinquencies & Household Debt Trends: What the New York Fed Data Show About Mortgage Risk

The health of the U.S. housing and mortgage market is deeply intertwined with how households manage their debt — including mortgages, credit cards, auto loans and student debt. The Federal Reserve Bank of New York’s Quarterly Household Debt and Credit reports provide timely, detailed data on balances, originations, delinquency transitions and credit-quality across debt types.

Digital Twins in Real Estate Valuation: The Next Appraisal Revolution

The real estate industry is undergoing one of its most significant technological shifts in decades — and at the center of this transformation is Digital Twin technology. As accuracy, speed, and transparency become essential in valuations, lenders, investors, and appraisal professionals are turning to digital replicas of physical properties to modernize the entire appraisal process.

Will Mortgage Rates Drop in 2026? Expert Forecast & Early Indicators

Mortgage rates have been one of the biggest challenges for both homebuyers and lenders over the past few years. After rising sharply due to inflation and aggressive Federal Reserve tightening, rates have remained stubbornly high—keeping buyers on the sidelines and reducing affordability across the U.S. market.

Tips for Homebuyers in a High-Rate Environment: Smart Strategies to Navigate Today’s Market

Mortgage rates in today’s market may feel challenging for buyers, but purchasing a home is still achievable with the right approach and preparation. Instead of waiting endlessly for rates to drop, homebuyers can adopt smarter strategies that improve affordability, protect long-term costs, and maximize financial stability.

Marketing Your Mortgage Business in a Digital-First World

The mortgage industry has shifted permanently into a digital-first environment. Borrowers are no longer just comparing rates — they are comparing experiences. They want faster applications, transparent communication, personalized guidance, and online convenience at every step.

Why Lenders Are Losing Money per Loan — and How Digital Tools Can Help

Over the past few years the cost to originate and deliver a mortgage has climbed sharply; many U.S. retail lenders are now losing money on a per-loan basis. The drivers are a mix of higher operational costs, longer warehouse/float times, repurchase and compliance risk, manual processes that don’t scale, and pressure on margins from market dynamics.

Mortgage Servicers & Borrower Default: What Happens When Things Go Wrong — Trends in 2025

Mortgage servicers play a critical role in the housing finance ecosystem: they collect payments, manage escrow, communicate with borrowers, and, importantly, handle problem loans when borrowers start to default. As the macroeconomic environment becomes more challenging in 2025, servicers are under increasing pressure.

Emerging Markets in Mortgage Lending: Non-Traditional Borrowers, Alternative Credit Data & Underserved Markets

As the U.S. housing industry evolves, so does the profile of today’s borrowers. Traditional credit models—once the backbone of mortgage underwriting—no longer capture the full picture of financial behavior.

The Changing Demographics of Homebuyers: Gen Z, Millennials, and How Their Buying Behavior Differs

After several years of volatile mortgage rates, 2025 is shaping up to be a major comeback year for refinance activity. As rates stabilize and dip slightly from their recent highs, millions of homeowners are re-evaluating their existing loans — creating a new wave of refinance demand that lenders, servicers, and mortgage tech providers must be ready to handle.

The Surge in Refinance Activity in 2025: What It Means for Your Business and Your Customers

After several years of volatile mortgage rates, 2025 is shaping up to be a major comeback year for refinance activity. As rates stabilize and dip slightly from their recent highs, millions of homeowners are re-evaluating their existing loans — creating a new wave of refinance demand that lenders, servicers, and mortgage tech providers must be ready to handle.

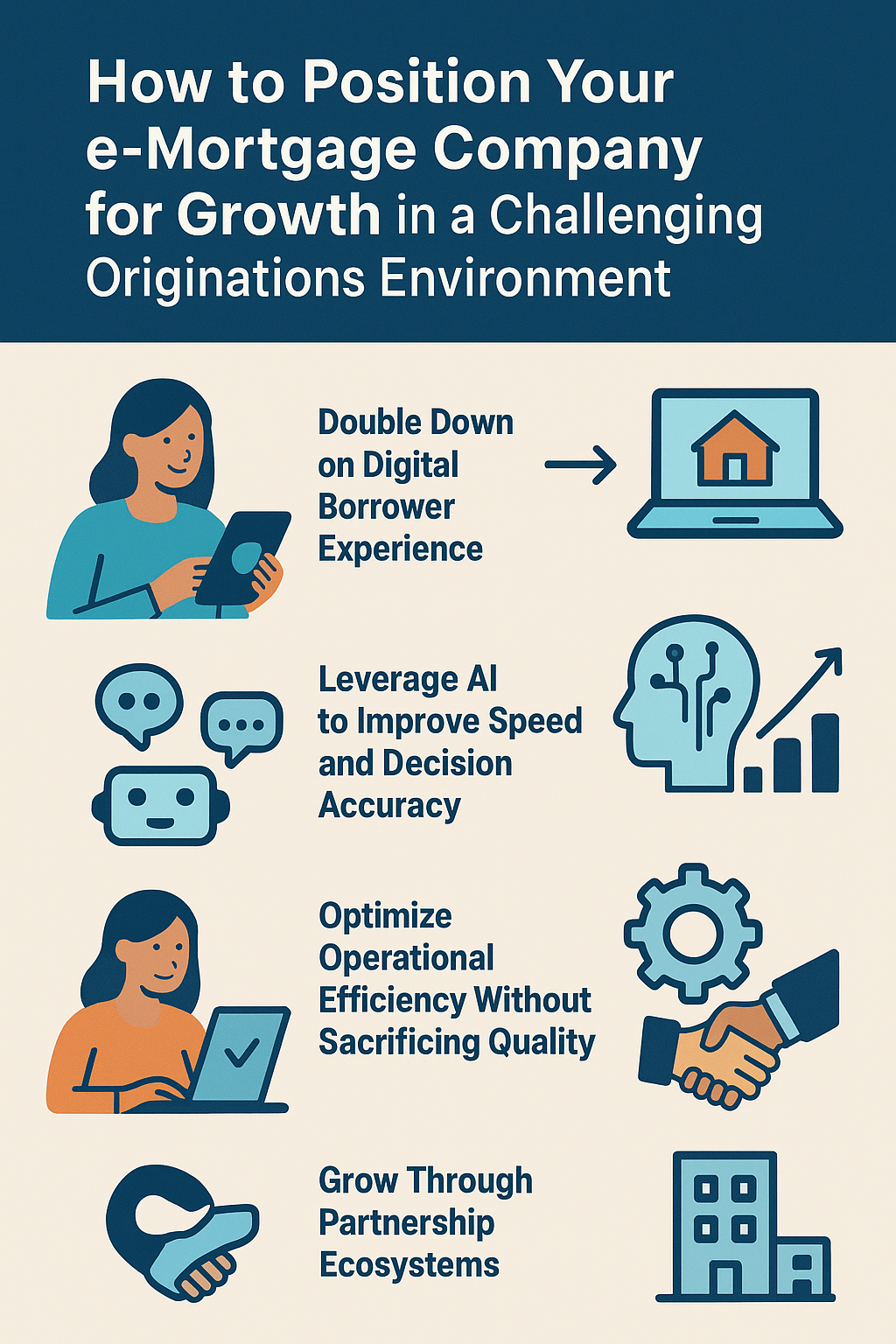

How to Position Your e-Mortgage Company for Growth in a Challenging Originations Environment

The mortgage industry continues to navigate one of the most complex and competitive environments in recent years. High interest rates, volatile housing demand, tighter lending guidelines, and rising customer expectations have created a challenging atmosphere for loan originations.

Inclusive Tech: Making eMortgages Accessible to All Borrowers

As the mortgage industry accelerates its shift toward fully digital experiences, one priority is rising to the forefront: inclusivity. eMortgage solutions promise speed, efficiency, and transparency — but these benefits only matter if every borrower can participate.

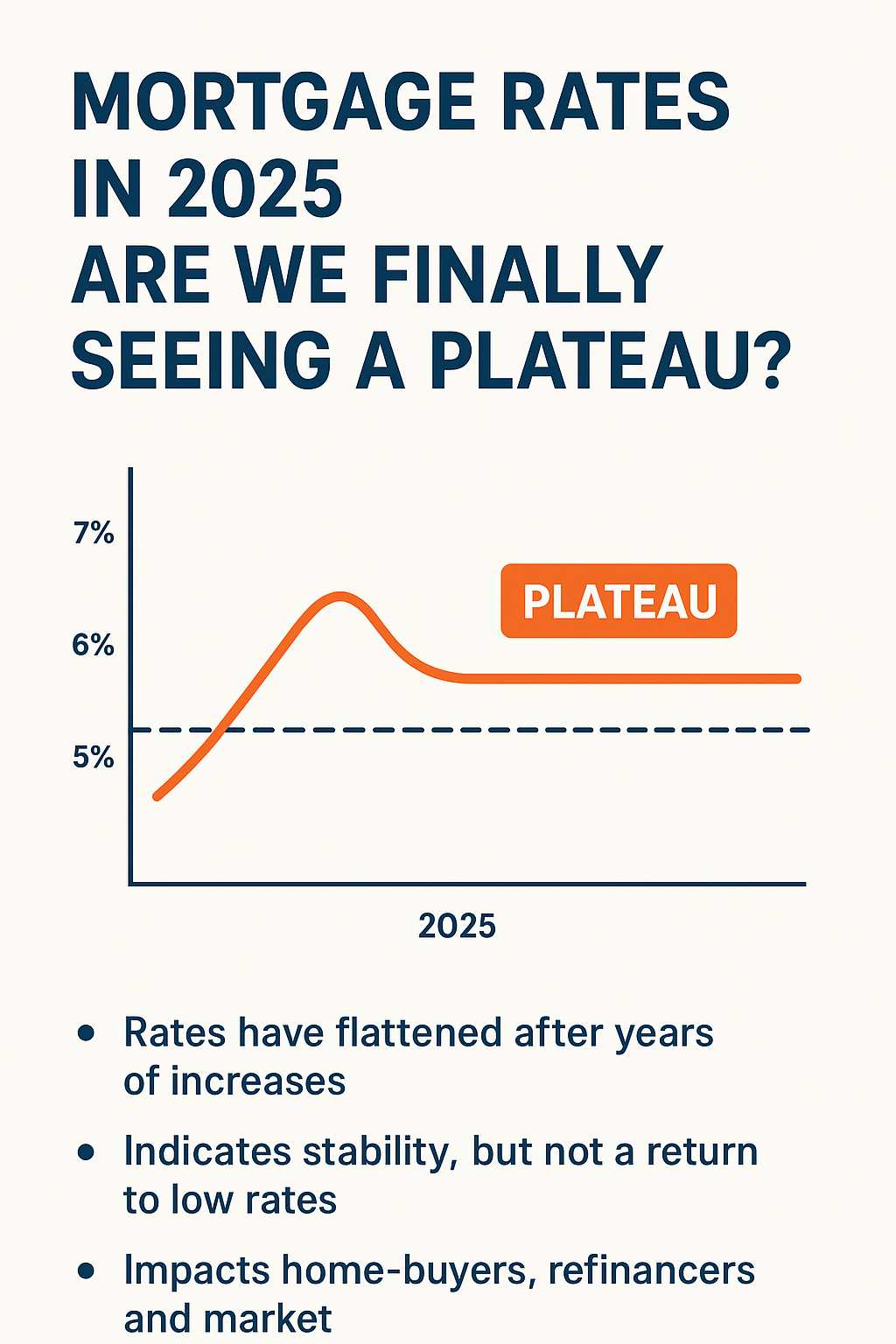

Mortgage Rates in 2025: Are We Finally Seeing a Plateau?

In 2025, mortgage rates in the U.S. appear to have entered a new phase. After a sharp rise in prior years, the benchmark 30-year fixed mortgage rate is no longer surging — instead, it seems to be flattening out. But what does a plateau really mean in this context? And what are the implications for home-buyers, refinancers and the broader housing market? This article breaks it down.

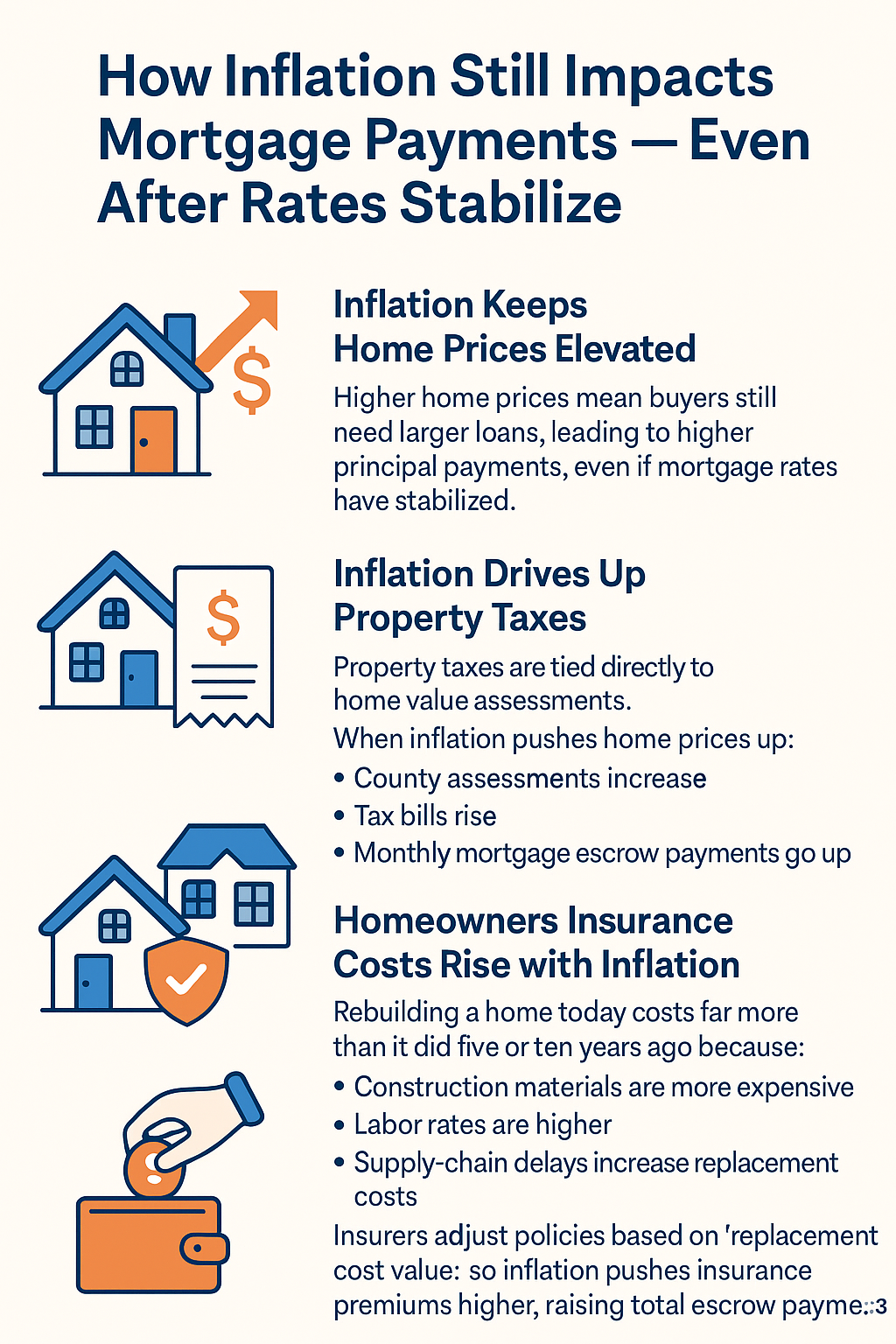

How Inflation Still Impacts Mortgage Payments — Even After Rates Stabilize

Inflation may finally be cooling in the U.S., and mortgage rates are beginning to level out after years of volatility. But for homeowners and buyers, the effects of inflation don’t disappear the moment interest rates stabilize.

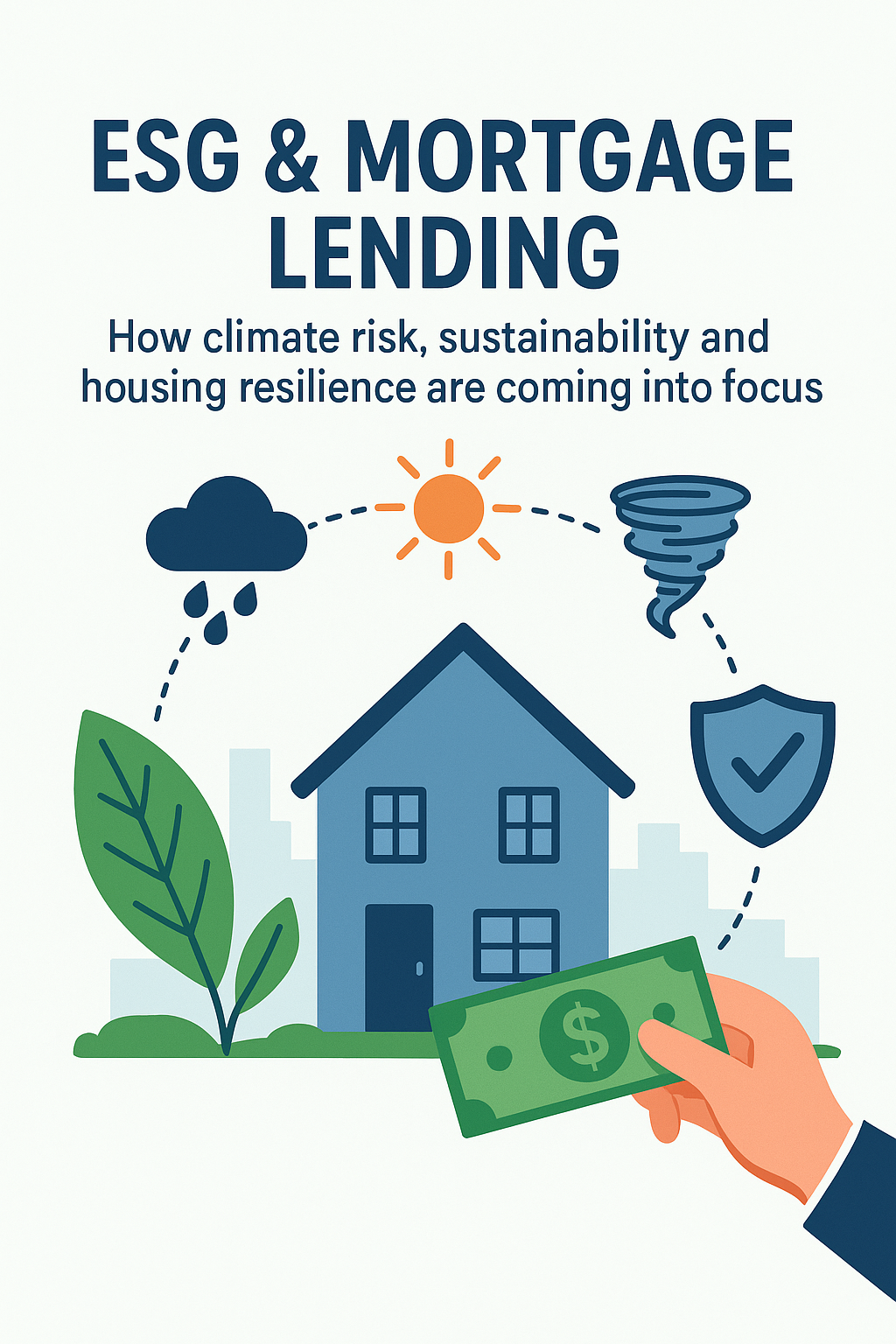

ESG & Mortgage Lending: How Climate Risk, Sustainability, and Housing Resilience Are Reshaping the Industry

As climate-related events intensify and sustainability expectations rise, the mortgage industry in the U.S. is undergoing a major shift. Environmental, Social, and Governance (ESG) considerations—once optional—are now becoming central to how lenders assess risk, price loans, and build long-term portfolio resilience.

Regional Spotlight 2025: The U.S. Markets Where Homebuying Is Still Feasible — and Where It’s Toughest

In 2025, the U.S. housing market remains defined by two realities: slightly higher home prices and mortgage rates that continue to hover above 6%. For buyers, affordability varies dramatically depending on where they shop — and for lenders, understanding these regional shifts is critical to guiding borrowers and capturing purchase volume.

Regional Spotlight: The U.S. Cities Still Affordable for Homebuyers

With mortgage rates elevated and housing inventory tightening in many major metros, affordability has become one of the biggest challenges for U.S. homebuyers. While coastal markets continue to dominate headlines with record-high prices, several regions across the country still offer attainable homeownership opportunities—with stable markets, strong job growth, and better price-to-income ratios.